Planning today to protect tomorrow: Retirement preparations among today's youth

-

61.3% of Gen Zs are taking steps to financially secure their futures.

Planning for retirement is crucial, even for younger generations. While understanding savings and investments is essential, it’s just the starting point. In this article, we delve into young people’s perspectives on saving for their future and how they approach it, based on insights from our Global Consumer Study.

The economic significance of retirement savings ensures that pension funding is never far down the political agenda. Indeed, proposed pension reform in France in 2023 saw wide-scale strikes and social unrest documented in media outlets around the world.

However, the models adopted in the markets in our survey vary considerably both in their structure and accessibility.

For younger generations, retirement may seem like a distant prospect. Nevertheless, there is evidence that Gen Zs and Millennials are actively preparing for their future, whether through personal or employer-based pension schemes, or through their own investments and savings.

Pushing up pension savings

Several trends are likely to be behind an increasing necessity to save for the future. Over recent decades, increasing life expectancies have prompted some governments to shift more of the onus for funding retirement from the state to the individual. Furthermore, those trends in longevity are a likely contributing factor to the diminishing significance of defined benefit pension plans.

The OECD’s Pension Markets in Focus 2022 report [13] highlights some of the different models in place around the world. These include mandating employees to join a private pension, which is the case in Chile, and Mexico; requiring employers to offer an automatic enrolment pension but allowing employees to opt out, which has been adopted by the UK. Elsewhere, there are models such as that adopted in Singapore that require all employees to contribute a significant proportion of their earnings to the Central Provident Fund.

Preparation priorities

Breaking down the findings by age shows how planning priorities change as the recognition dawns that retirement is not just a distant possibility, but an approaching life stage that requires considerable funding.

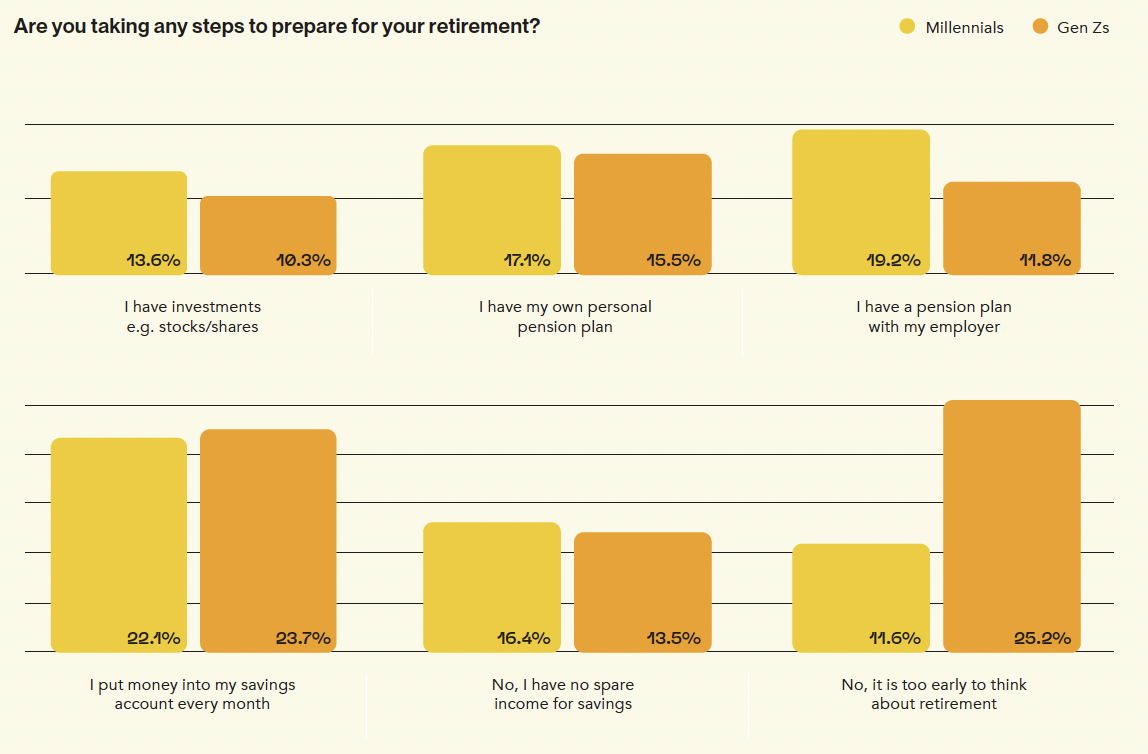

Unsurprisingly, engagement levels vary considerably by generation. Amongst Gen Z respondents, a quarter (25.2%) believe that it is still too early to think about retirement, compared with <12% of their elder counterparts. The main reason for Millennials not making preparations for their retirement is a shortage of spare income (16.5%).

Nevertheless, many young people are still seeing the value in contributing to pensions. According to our survey, over a third (36.3%) of Millennials have either a personal or employer pension plan, while the figure slightly decreases to 27.3% for Gen Zs. The disparity will be impacted by the fact that more than a fifth (21.9%) of Gen Z respondents are still in full-time education and therefore do not qualify for an employer pension plan yet.

A second influencing factor may be minimum entry ages to many employer schemes, which might rule out many Gen Zs. Where this is so, it is likely to reinforce the view of that generation that it is too early to plan for retirement.

Also noteworthy is the contrast in the preparations made by respondents from different markets. In the UK & ROI, a higher percentage (37%) contribute to pension schemes compared to the rest of Europe (29.2%). However, the situation is reversed for investments and savings, with only a quarter (24.7%) of the youth in the UK & ROI paying into savings accounts, while a third (32.5%) of those in the rest of Europe do so.

While this discrepancy may be partly attributed to the presence of auto-enrolment pension schemes in the UK, which is only prevalent in a small handful of European markets, it also brings attention to the potential influence of cultural differences on young people’s financial planning preferences.

Pension literacy

Insurers are well-positioned to support young people with education around financial planning. Pensions is the product area where our respondents have the least knowledge – 17.6% say they have no knowledge at all and a further 38.8% say their understanding is limited.

This lack of knowledge is understandable. Pension provision is a highly complex area of financial planning requiring an understanding of state provision (if any) and of the regulatory landscape of private or employer-sponsored schemes.

By comparison, young people have a lot more confidence in their understanding of savings products, with 69.3% claiming a good or very good level of knowledge here. It is conceivable that savings products are more heavily promoted towards Gen Zs and Millennials than pension products, which may be seen with less urgency by this audience.

To improve pension knowledge, early engagement is key to the best possible outcome at retirement. Providing financial education could help raise awareness and ensure that retirement planning is given the priority that it needs and deserves.

To further demonstrate value, providers may benefit from emphasising the significant weight of employer contributions some markets mandate for pensions, a benefit not felt in other areas of investment.

But even armed with good knowledge about a product – as in savings – it should be remembered that knowledge is only a first step on this journey.

It's also about timing

With so much discussion about what type of retirement planning young people are making, it is easy to miss the elephant in the room – sometimes young people simply aren’t willing or able to make any future plans yet.

This year’s data shows that, although almost half of young people in China are making some form of pension payment (49.5%), the figure drops to a fifth (20.7%) for Japan. In fact, 29.7% of Japanese respondents told us they weren’t preparing for retirement in any way because they simply had no spare money to save, invest or pay into a pension scheme.

For insurers, the lesson here is to meet young people where they are, not where we would like them to be. It is a reminder that young people may need to be supported in other ways first, and that stress around work and financial uncertainty (Insight 4) may need to be addressed before financial planning can be endeavoured.

Key Findings

- Nearly 70% of respondents are putting something away for the future. This could be into a pension (33.1%), investments (12.5%) or savings (22.6%).

- But a quarter of Gen Zs (25.2%) around the world aren’t making preparations because they consider it too early to do so with a further 13.6% not doing so because of a lack of spare income.

- The greatest number of young people making some form of financial preparation for their retirement are found in Taiwan (90.2%), Hong Kong (86.1%) and Singapore (83.5%), while Australian (51.7%), Spanish (54.2%) and Chilean (56.5%) respondents are taking least action.

References

[13] OECD. (2022). Pension Markets in Focus 2022. [Online]. OECD.org. Available at: https://www.oecd.org/finance/p... [Accessed 21 June 2023].