Mapping out the insurance journey (Part 2)

In this article, we look into the second part of Insight Two from our Global Consumer Study. We explore the communication preferences of Gen Zs and Millennials with insurers, as well as whether they feel inclined to stick with current policies or explore offerings from different insurers.

Beyond the purchase – happy ever after?

As we have remarked so often, insurance is not a purchase to quicken the pulse. Once bought it sits patiently and largely unnoticed until or unless the fateful day arrives when it is called into action. So, the purchase process is a rare opportunity to make a lasting impression.

As a test of how well the industry is doing, we asked those participants who had purchased insurance in the last two years to give star ratings out of 5 to various aspects of the process. From the results it would seem that the industry is doing a good job – either that or young people are extraordinarily generous with their ratings!

At first sight, by far the least satisfied with their experience were the Japanese. Taking customer service as an example, just 16% awarded 5 stars in respect of their P&C experience and a little under 19% for L&H. However, 4-star ratings were very much in line with the averages across all markets. One is inclined to suspect that cultural differences are playing a part.

Customer communication

The challenge for insurers is to build on this promising start and build brand loyalty with their customers. One way is by regular communication. But this, again, can be a double-edged sword – approaching customers too often or with unwanted information is likely to be a cause of irritation rather than appreciation. The survey sought guidance on what types of content would be of interest. It appears that Gen Zs are more receptive to educational content than their Millennial counterparts. But it is clear that communications that might bring some financial benefit sparked the most interest – money management tips and information about discounts and offers.

There is relatively little appetite for company news.

Those who expressed interest about receiving more information about any of the topics were also asked for their preferred delivery method.

Perhaps surprisingly, for these digitally-focused generations, the most favoured option is the relatively old technology of the email. This is perhaps a recognition that an email may still be the best medium for detailed content.

Claims

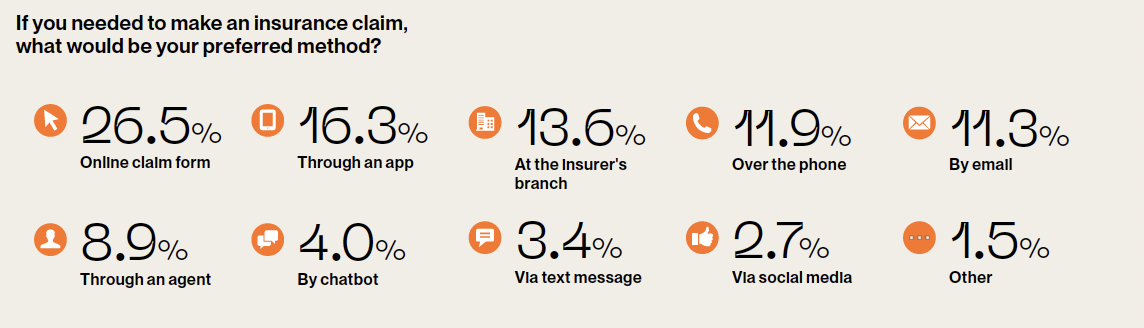

The way in which claims are handled presents an opportunity for insurers to cement their relationship with a client. Equally importantly, a satisfied claimant is a potential ambassador in a business where, as we have seen, personal recommendations have a significant influence. Of course, it can also be a potential point of conflict if the claim is somewhat speculative or if it is not strictly covered under the policy conditions. However, any steps that insurers take to make the process as user-friendly as possible will earn the appreciation of customers.

Participants were asked to indicate their preferred way to register a claim should the need arise. There is a strong preference for online and digital channels, but more traditional methods, such as in-branch or by phone, still command a significant following. One suspects the preferences would be yet more equally divided if one were to include the preferences of older generations. This underlines the importance of continuing to offer a choice of routes to fit the needs of different sectors of the customer base.

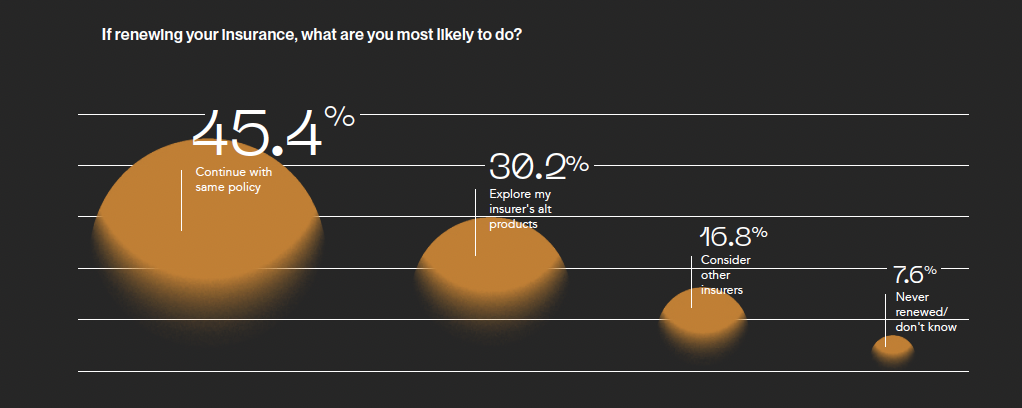

Renewal

For policies issued on a renewable basis, policyholder actions could be considered to be an indication of customer satisfaction. Our survey reveals that there is evidence either of considerable levels of satisfaction or simply inertia. That despite the wealth of information available to the younger generations through digital media. Around 45% would continue with the same policy and only 17% would consider products from other insurers.