Mapping out the insurance journey (Part 1)

In this latest article, we delve into the second insight of our Global Consumer Study, focusing specifically on the insurance purchase triggers for Gen Zs and Millennials. Here, we explore what is most appealing to the younger generations when considering potential insurers.

#1 consideration during the purchase process is "good online reviews" – more so than price.

Buying insurance is not what most have in mind when they think of "retail therapy". The products rarely if ever evoke excitement or pride of ownership. Nevertheless, nearly 85% of our survey participants have at least one P&C product and close to 80% have a L&H insurance policy.

What is it that has prompted our digital generations to buy insurance when, no matter how advisable insurance may be, there are so many more exciting products and services to claim their attention?

Our survey sought to find answers.

We asked respondents about their most recent purchase of both P&C and L&H products. We asked them what prompted their path to purchase; how they went about gathering advice and information, and about the factors influencing their choice of insurer.

Purchase triggers

Our questioning quickly dispelled any notion that young people simply have warm and fuzzy feelings towards insurance. Two-thirds of the most recent purchases of P&C products and nearly two-fifths of L&H purchases were mandatory. This might be where insurance is required by law – for example motor insurance or perhaps required as a condition of another transaction, such as home or life insurance in conjunction with a mortgage.

When it comes to discretionary purchase of insurance, it is interesting to see that time-tested family and friend recommendations are the single biggest trigger for both P&C and L&H purchases, for these age groups.

Furthermore, when we look at the responses by generation group, we see that Gen Zs are even more likely to be influenced by family and friends than Millennials.

However, the influence of digital media cannot be ignored. Social media (15.5%) and online or TV advertising (15.1%) are significant purchase triggers, particularly so for P&C products and noticeably more so for Gen Zs than Millennials.

Financial advisers continue to play a major role in generating L&H purchases, but hold very much less sway in the P&C market.

Gen Zs and Millennials value the opinions of their friends and family highly.

Global Consumer Study 2023-24.

Sources of advice and information

Family and friends continue to have a major influence in the next stage of the purchase journey in providing advice and information (34% for P&C; 33% for L&H). The aggregate of the responses indicates that consumers are even more likely to seek professional advice from insurance agents or financial advisers (43% for P&C; 65% for L&H), but as we shall see below there are generational differences.

In addition, a significant proportion of respondents conducted research online (37% for P&C; 27% for L&H). When we examine the key sources they turn to for advice, we see a generational paradox. Gen Z respondents, arguably the most digitally literate of the generations, are less likely to research online than Millennials. Equally Gen Zs are less likely to turn to professional advice than Millennials.

Choice of insurer

We now know something of how younger consumers go about gathering advice and information, but what is it that they are looking for? What is it that would attract them to a potential insurer?

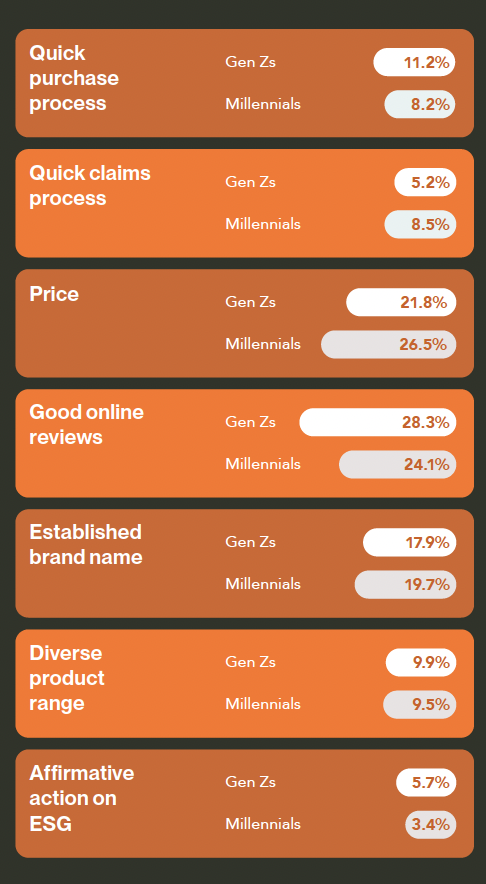

Our survey participants were asked which features would be most important to them when selecting an insurer. It is striking that for the digital generations, good online reviews are as important – and more important for Gen Z respondents – than price. It is a fact that underlines the dividend to be gained from good customer service and conversely, the penalty to be paid for failing to meet expectations. Customer experience can be shared very quickly and widely online – a double-edged sword for insurers!

It seems that reputations for action on environmental, social and governance issues are not a significant factor in the purchase decision for these generations. This should not be interpreted as a sign that these matters are of no importance. In all probability, it reflects the practical difficulty of making an objective judgment of the competing merits of insurers.

Respondents appear to be drawn to established brands but nonetheless are open to the possibility of buying from new online companies that have recently entered the market.

Over 50% would be willing to forsake brand reputation if the new online competition were cheaper or more convenient.

Time to commit

The research is done; the choices made, now how much attention is paid to the documentation before completion? We asked respondents the extent to which they read the fine print. There are no significant differences between responses by generation, but a huge diversity of responses from different markets.

By far the most diligent are the Indonesians 48.2% of whom claim to read the documentation in detail. Following them are the Chinese, 38.9% of whom claim to read the fine print. The French sit firmly at the relaxed end of the spectrum. 22.2% just sign without a further thought and only 12.2% review documents in detail. Somewhat surprisingly, the Japanese show a similar level of disinterest in the detail. 19.4% just sign and only 11.8% - even fewer than the French – look at the detail.

Key Findings

- Gen Zs and Millennials value the opinions of their friends and family when purchasing insurance. But, with many checking out online reviews too, their circle of influence is wide. Positive online reviews is the top feature when purchasing insurance, especially among younger people. Price becomes the priority as they age.

- Customer service and the quality of information provided during the application process score highly with younger generations. The complexity of applying remains an irritation.

- Despite a wealth of information available to the younger generations through digital media, around 45% would continue with the same policy and renew it.